If you’ve ever felt a shift in your financial world—a sudden jump in your mortgage quote, a change in your car loan’s interest rate, or finally, a glimmer of meaningful growth in your savings account—you’ve likely felt the ripple effect of a single, powerful number: the federal funds rate.

Set by the Federal Reserve (the Fed), the U.S. central bank, this rate is the cornerstone of American monetary policy. While it might seem like an abstract concept discussed by economists on financial news networks, its influence is profoundly personal. It directly dictates the cost of borrowing money and the reward for saving it, touching nearly every aspect of your financial life.

This article will demystify the federal funds rate. We will trace its journey from a decision made in a boardroom in Washington, D.C., to its tangible impact on your wallet, explaining how it affects your mortgage, your car loan, and your savings account. By understanding this ripple effect, you can make more informed financial decisions, anticipate market trends, and navigate the economic currents with greater confidence.

Part 1: The Source of the Ripple – Understanding the Federal Funds Rate

What Exactly is the Federal Funds Rate?

At its core, the federal funds rate is the interest rate at which depository institutions (like commercial banks and credit unions) lend their excess reserves to each other on an overnight, unsecured basis. These transactions help banks meet their reserve requirements—the minimum amount of cash they must hold in their vaults or at the Federal Reserve.

Think of it as the “wholesale” price of money between banks. It’s the foundational cost of short-term capital for the financial system. The Fed does not dictate this rate by fiat; rather, it sets a target range and uses its powerful monetary policy tools to push the market rate into that desired range.

The Conductor of the Economy: The Federal Reserve

The Federal Reserve, often called “the Fed,” has a dual mandate from Congress: to foster maximum employment and to maintain stable prices (i.e., control inflation). The federal funds rate is its primary instrument for achieving these goals.

The decision on where to set the rate is made by the Federal Open Market Committee (FOMC), which meets eight times a year. During these meetings, they analyze a vast amount of economic data—employment figures, consumer spending, inflation metrics, global economic conditions, and more—to determine whether to raise, lower, or hold the rate.

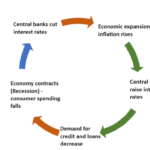

- To Stimulate a Weak Economy: If the economy is slowing down, unemployment is rising, and inflation is low, the Fed will typically lower the federal funds rate. This makes it cheaper for banks to borrow, encouraging them to lend more freely to businesses and consumers at lower rates. This stimulates spending, investment, and hiring, acting as an accelerator for the economy.

- To Cool Down an Overheating Economy: If the economy is growing too quickly, leading to high inflation (where the prices of goods and services are rising rapidly), the Fed will raise the federal funds rate. This increases the cost of borrowing for banks, which in turn charge higher rates on loans to their customers. This discourages spending and slows down the economy, tapping the brakes to prevent inflation from spiraling out of control.

This delicate balancing act is why the Fed’s decisions are so closely watched. Getting it wrong—stimulating for too long or tightening too aggressively—can lead to recessions or prolonged periods of high inflation.

Part 2: The First Major Ripple – How the Fed Rate Impacts Mortgage Rates

For most people, a mortgage is the largest debt they will ever take on. The difference of even half a percentage point in your mortgage rate can translate to tens of thousands of dollars over the life of the loan. The federal funds rate is a key driver of these changes, but the relationship is indirect and nuanced.

The Link: The 10-Year Treasury Note

Mortgages are long-term loans, typically 15 to 30 years. Therefore, they are not directly tied to the overnight federal funds rate. Instead, mortgage rates, particularly for the standard 30-year fixed-rate loan, are closely correlated with the yield on the 10-year U.S. Treasury note.

Here’s the connection:

- When the Fed raises the federal funds rate, it signals that it is committed to fighting inflation. This often leads to higher yields on long-term government bonds like the 10-year Treasury, as investors demand a higher return to compensate for the inflationary environment and the higher rates available on short-term debt.

- Banks and other lenders use the 10-year Treasury yield as a benchmark. To make a profit, they set mortgage rates at a premium to this “risk-free” rate. The spread between the 10-year yield and the average 30-year mortgage rate accounts for the lender’s profit, the risk of the loan, and servicing costs.

So, while a Fed rate hike doesn’t automatically cause a 1:1 increase in your mortgage rate, it sets off a chain reaction in the bond market that almost always pushes mortgage rates higher.

A Tale of Two Mortgage Types

- Fixed-Rate Mortgages: If you already have a fixed-rate mortgage, changes in the Fed funds rate do not affect your monthly payment. You locked in your rate at closing, and it remains constant. However, if you are planning to buy a new home or refinance an existing one, the current environment is critical. A rising rate environment means new fixed-rate mortgages will be more expensive.

- Adjustable-Rate Mortgages (ARMs): ARMs are directly and immediately sensitive to changes in the federal funds rate. ARMs are typically tied to a short-term benchmark index like the Secured Overnight Financing Rate (SOFR) or the Prime Rate, which moves in near lockstep with the Fed’s actions.

- If you have an ARM, your initial rate is fixed for a set period (e.g., 5, 7, or 10 years). After that, it adjusts periodically (e.g., annually). When the Fed raises rates, the index to which your ARM is tied goes up, and your next adjustment will likely result in a higher monthly payment. This can create significant payment shock for homeowners.

Practical Scenarios:

- Fed in Hiking Mode (2022-2023): As the Fed aggressively raised rates to combat post-pandemic inflation, the average 30-year fixed mortgage rate soared from around 3% to over 7%. This dramatically increased monthly payments for new homebuyers, cooling a red-hot housing market. A person with a $500,000 loan saw their monthly principal and interest payment jump from about $2,100 to over $3,300.

- Fed in Cutting Mode (2020): In response to the COVID-19 pandemic, the Fed slashed the federal funds rate to near zero. Mortgage rates followed, plummeting to historic lows. This triggered a massive refinancing boom and fueled a surge in home buying, as the cost of borrowing became incredibly cheap.

Part 3: The Second Ripple – Car Loans, Credit Cards, and Other Consumer Debt

While mortgages are influenced by long-term rates, most other consumer debt is directly tied to short-term interest rates, making them more immediately reactive to the Fed’s decisions.

The Key Transmission Vehicle: The Prime Rate

The Prime Rate is the interest rate that commercial banks charge their most creditworthy corporate customers. It is almost perfectly correlated with the federal funds rate; when the Fed moves, the Prime Rate typically follows within days. The standard formula is: Prime Rate = Federal Funds Rate + 3%.

This Prime Rate becomes the baseline for a wide array of consumer lending products.

Car Loans

Financing a vehicle involves either a direct loan from a bank or credit union or indirect financing through the automaker’s captive finance company (e.g., Ford Credit, Toyota Financial Services).

- Bank Loans: These are heavily influenced by the Prime Rate. When the Fed raises rates, banks’ cost of funds increases, and they pass this cost onto consumers through higher Annual Percentage Rates (APRs) on new and used car loans.

- Dealer Promotions: You’ve likely seen ads for “0% APR Financing.” These are subsidized rates offered by the manufacturers to move inventory. In a high-rate environment, these promotions become less common and more restrictive, as the cost to the manufacturer to offer them becomes prohibitive. Instead, you might see more cash-back offers.

The impact is direct: a higher interest rate on a $40,000, 5-year car loan can add $50-$100 or more to your monthly payment, making car ownership more expensive and potentially dampening consumer demand in the auto market.

Credit Cards

The vast majority of credit cards have a variable interest rate tied directly to the Prime Rate. Your cardholder agreement will state something like, “APR = Prime Rate + [a margin based on your creditworthiness].”

- When the Fed raises the federal funds rate, the Prime Rate rises, and your credit card’s APR follows suit, usually within one or two billing cycles.

- This makes carrying a credit card balance significantly more expensive. If you have a large balance, a series of Fed rate hikes can dramatically increase your monthly finance charges, making it harder to pay down the principal. This is one of the most immediate and painful effects of Fed tightening for the average consumer.

Other Consumer Loans

- Home Equity Lines of Credit (HELOCs): Like credit cards, HELOCs almost universally have variable rates tied to the Prime Rate. A Fed rate hike will directly increase the interest rate on your outstanding HELOC balance, raising your required monthly payments.

- Personal Loans: While some personal loans are fixed-rate, many, especially from online lenders, are variable. Even fixed-rate personal loans will see their average offered rates increase in a rising rate environment, as the lenders’ own cost of capital has gone up.

Part 4: The Silver Lining Ripple – Savings Accounts and Certificates of Deposit (CDs)

For years following the 2008 financial crisis, savers were frustrated. The Fed held rates near zero, and the interest earned on savings accounts and CDs was negligible—often a fraction of a percent. This dynamic changes dramatically when the Fed begins raising rates, creating a significant benefit for savers.

How It Works: Banks’ Incentive to Attract Deposits

When the federal funds rate is high, banks can earn a better return by lending money to other banks or to customers at these higher rates. To have more money to lend, they need to attract deposits. They do this by offering more competitive interest rates on their savings products.

- High-Yield Savings Accounts (HYSAs): These are the most responsive to Fed rate hikes. Online banks, which have lower overhead than traditional brick-and-mortar banks, are often the first to raise their APYs (Annual Percentage Yields). It’s not uncommon for HYSAs to offer yields that are multiple times the national average, closely tracking the upward movement of the federal funds rate.

- Money Market Accounts (MMAs): Similar to HYSAs, MMAs become much more attractive in a high-rate environment. They often come with check-writing privileges and debit card access, making them a flexible place to park emergency funds while earning a respectable return.

- Certificates of Deposit (CDs): CDs are time deposits where you agree to lock up your money for a specific term (e.g., 6 months, 1 year, 5 years) in exchange for a fixed interest rate. In a rising rate environment, banks must offer higher rates on new CDs to attract customers. This can be a great opportunity to lock in a guaranteed return, but there is a risk: if you lock in a 2-year CD and rates continue to rise, you’ll miss out on those even higher yields. A common strategy in this scenario is “CD laddering,” where you spread your investments across multiple CDs with different maturity dates.

The Saver’s Opportunity:

The shift from a near-zero rate environment to a higher one is a paradigm shift for savers. It transforms cash and cash-equivalents from a losing asset (after accounting for inflation) to a viable, low-risk component of a diversified portfolio. It provides a safe way to grow your emergency fund and short-term savings goals without taking on market risk.

Navigating the Ripples: Proactive Financial Strategies

Understanding the ripple effect is only half the battle. The other half is using this knowledge to make smarter financial moves.

In a Rising Rate Environment:

- Prioritize paying down high-interest debt. Credit cards and variable-rate loans will become increasingly expensive. Focus your extra cash on eliminating these balances.

- Lock in a fixed rate if you have a variable-rate debt like an ARM or HELOC, if possible, by refinancing into a fixed-rate product.

- Shop around for high-yield savings accounts. Don’t let your cash languish in a traditional savings account paying 0.01% APY. Move your emergency fund to an HYSA to maximize your return.

- Consider CDs to lock in attractive rates for your medium-term savings, but be mindful of the interest rate trajectory.

- Be prepared for a cooler job market. The Fed raises rates to slow the economy, which can lead to slower hiring or even layoffs. Bolster your emergency fund.

Read more: Bond Market Blues: Why Treasury Yields are the Key to Understanding Equity Volatility

In a Falling Rate Environment:

- Consider refinancing your mortgage. If you have a high-rate mortgage, a falling rate environment is your opportunity to reduce your monthly payment and total interest cost.

- It’s a good time to finance a large purchase. Look for lower rates on car loans, home renovations, or other major expenses.

- Be cautious about locking money into long-term CDs, as you might get stuck with a below-market rate if yields continue to fall.

- Understand that savings account yields will drop. The high yields on HYSAs will gradually decline, so you may want to lock in longer-term CDs if you suspect rates have peaked.

Conclusion: Empowering Yourself Through Financial Literacy

The federal funds rate is far more than an esoteric economic indicator. It is a powerful force that creates a cascade of effects, influencing the cost of your home, your car, and your credit card debt, while simultaneously determining the growth of your hard-earned savings.

By understanding this “ripple effect,” you transition from a passive observer to an active manager of your financial well-being. You can anticipate changes, understand the financial news with greater clarity, and make strategic decisions that align with the broader economic currents. While you cannot control the decisions of the Federal Reserve, you can absolutely control how you respond to them. Use this knowledge to build a more resilient, proactive, and successful financial future.

Read more: The Dollar’s Dominance: How a Surging USD is Impacting Multinationals

Frequently Asked Questions (FAQ)

Q1: If the Fed just raised rates, why is the APR on my savings account still so low?

There’s often a lag, and not all banks are created equal. Large traditional brick-and-mortar banks, flush with deposits, have little incentive to quickly raise rates for existing customers. They often rely on customer inertia. Actionable Step: Be proactive. Online banks and credit unions are much more competitive. It takes minimal effort to open a High-Yield Savings Account (HYSA) and transfer your funds to start earning a much better return.

Q2: I have a fixed-rate mortgage and no credit card debt. Does the Fed’s action affect me at all?

Yes, albeit more indirectly.

- Home Equity: If rising rates cool the housing market, the rate of appreciation of your home’s value could slow, or prices could even fall, affecting your net worth.

- Investments: Rising rates can negatively impact the stock and bond markets. Companies face higher borrowing costs, which can hurt profits, and bond prices have an inverse relationship with interest rates.

- General Economy: The Fed’s goal in raising rates is to slow down the entire economy. This can impact your job security, business revenue, and the overall health of the community you live in.

Q3: How quickly do credit card rates change after a Fed announcement?

Very quickly. Since credit card rates are variable and tied to the Prime Rate, which moves almost immediately after a Fed change, your new, higher rate will typically take effect within one or two billing cycles. Your cardholder agreement will specify the exact terms.

Q4: What’s the difference between the Federal Funds Rate and the “Discount Rate”?

This is a common point of confusion.

- Federal Funds Rate: The rate banks charge each other for overnight loans.

- Discount Rate: The rate the Federal Reserve charges banks for short-term emergency loans directly from the Fed’s “discount window.”

The Fed sets both, but the discount rate is usually set slightly higher than the funds rate to encourage banks to borrow from each other first.

Q5: Should I wait to buy a house or a car if I think rates might go down soon?

This is a classic “timing the market” dilemma.

- For a House: It depends on your local market and personal circumstances. If rates are high but expected to fall, you could be faced with high monthly payments initially, with the hope of refinancing later. However, if rates drop, demand for homes could surge, pushing prices higher and potentially offsetting the benefit of a lower rate. The best advice is to make a purchase decision based on what you can afford now and what fits your life, not solely on predicting interest rates.

- For a Car: It’s generally less consequential than a mortgage. If you need a car now, shop for the best available loan rate. If your current vehicle is fine and you believe rates will drop soon, waiting a few months is a lower-risk strategy.

Q6: Where can I find reliable, up-to-date information on the Fed’s actions?

Go directly to the source for the most authoritative information:

- The Federal Reserve Website (FederalReserve.gov): For FOMC statements, meeting calendars, minutes, and speeches by Fed officials.

- Board of Governors of the Federal Reserve System: For educational resources and official press releases.

Reputable financial news outlets (e.g., The Wall Street Journal, Bloomberg, Reuters) provide excellent analysis and commentary on these primary sources.