For millions of Americans, the housing market is more than just charts and data points; it’s the stage for their most significant financial decisions and personal aspirations. Yet, since the whirlwind of 2020-2021, that stage has undergone a profound transformation. The frenzied bidding wars have been replaced by a palpable standoff, a “chill” that has settled over both buyers and sellers. This isn’t a typical market correction nor a crash in the classical sense. It is a unique and complex phenomenon, born from a historic collision of macroeconomic forces, pandemic-era distortions, and deep-seated structural shifts.

To understand the current “housing market chill,” one must move beyond headlines and analyze the intricate dance between two primary forces: home sales volume and mortgage rates. This article will dissect this relationship, exploring the data, the human stories behind the numbers, and what the future may hold for the American dream of homeownership.

Part 1: The Pre-Chill Frenzy – A Perfect Storm of Demand

To appreciate the current freeze, we must first recall the heat of the recent past. The period from mid-2020 through much of 2021 was one of the most competitive housing markets in U.S. history. This frenzy was not accidental; it was the result of a “perfect storm” of converging factors:

- Pandemic-Driven Spatial Re-evaluation: With remote work becoming a widespread reality, millions of urban dwellers sought larger homes, home offices, and outdoor space. This triggered a massive migration, both to the suburbs and to more affordable Sun Belt states.

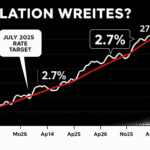

- Historic Low Mortgage Rates: In response to the economic shock of COVID-19, the Federal Reserve slashed interest rates to near-zero. This pushed the average 30-year fixed mortgage rate to all-time lows, bottoming out below 2.7% in late 2020 and early 2021. For a buyer, this dramatically increased their purchasing power, allowing them to bid on more expensive homes without increasing their monthly payment.

- Demographic Tailwinds: The large Millennial generation was hitting its prime home-buying years, creating a powerful demographic wave of demand.

- Limited Inventory: The supply of homes for sale was already low pre-pandemic. The sudden surge in demand rapidly depleted this inventory, leading to a record-low number of homes available for sale.

The result was a blistering pace of home sales. Existing-home sales peaked at a seasonally adjusted annual rate of 6.73 million in January 2021. Prices soared at a double-digit annual pace, with the S&P CoreLogic Case-Shiller U.S. National Home Price Index rising over 19% year-over-year in 2021. It was a seller’s market of epic proportions.

Part 2: The Big Shift – The Mortgage Rate Hammer Drops

The catalyst for the “chill” was the most powerful tool in the macroeconomic arsenal: interest rates. As inflation surged to 40-year highs in 2022, the Federal Reserve embarked on the most aggressive monetary tightening cycle since the 1980s. The Fed does not directly set mortgage rates, but its policy rate influences the yield on the 10-year Treasury note, which is the primary benchmark for 30-year fixed mortgages.

The effect was swift and severe. The average 30-year fixed mortgage rate, as tracked by Freddie Mac, began a precipitous climb:

- End of 2021: ~3.1%

- End of 2022: ~6.4%

- Peak in October 2023: ~7.8%

In less than two years, the cost of financing a home had more than doubled. This single variable fundamentally reshaped the entire housing market calculus.

The Data: A Market in Lockdown

The impact on home sales volume has been dramatic and consistent. According to the National Association of Realtors (NAR), existing-home sales, which account for the vast majority of the market, have fallen sharply from their 2021 peak.

- The Decline: By the first quarter of 2024, existing-home sales had dropped to a seasonally adjusted annual rate of approximately 4.2 million, a decline of nearly 40% from the peak.

- The Lock-in Effect: Perhaps the most defining characteristic of this chill is the “lock-in effect” or “golden handcuffs.” Homeowners who secured a mortgage rate at or below 3% are now extremely reluctant to sell. Why? Because doing so would mean trading their ultra-low monthly payment for a new one that could be 50-100% higher on a similarly priced home. This has frozen a significant portion of the existing housing stock, crippling inventory. Data from the ICE Mortgage Technology report shows that as of early 2024, over 60% of all outstanding mortgages had an interest rate below 4%.

This creates a vicious cycle:

High Rates → Fewer Sellers (Lock-in Effect) → Low Inventory → Sustained High Prices → Fewer Buyers (Affordability Crisis) → Low Sales Volume.

Part 3: The Great Standoff – Buyers vs. Sellers in a Frozen Market

The current market is best described as a high-stakes standoff between two exhausted parties.

The Buyer’s Plight: The Affordability Abyss

For buyers, the math is brutal. Let’s illustrate with a simple example:

- January 2021: A $500,000 home with a 20% down payment and a 2.7% mortgage rate results in a principal and interest payment of approximately $1,620 per month.

- October 2023: That same $500,000 home with a 20% down payment and a 7.8% mortgage rate results in a monthly payment of approximately $2,880.

Even though home price growth has cooled in many markets, it has not fallen nearly enough to offset the rate-driven payment shock. According to the NAR, the monthly mortgage payment on a typical existing single-family home with a 20% down payment has more than doubled since the end of 2019. This has pushed the median payment as a percentage of median family income to levels not seen since the peak of the housing bubble in the mid-2000s, decimating affordability.

First-time buyers, who don’t have existing home equity to leverage, are particularly hard-hit. They are competing for a scarce supply of entry-level homes against investors and all-cash offers, which now make up a larger share of a shrinking pie.

The Seller’s Paradox: The Prison of a Low Rate

On the other side, sellers are trapped by their own good fortune. A family that might normally “trade up” to a larger home now faces a financial disincentive too large to ignore. Selling their $400,000 home to buy a $600,000 one is no longer a simple matter of a slightly higher payment; it’s a quantum leap. This has led to a peculiar phenomenon: the market is seeing a rise in “equity-rich” homeowners who are, in practice, “payment-poor” in terms of their ability to move.

This is why new construction has, in some markets, taken on an outsized role. Homebuilders, unlike existing homeowners, are not locked in by a low mortgage. They have inventory to sell and have been aggressively using mortgage rate buydowns as an incentive, effectively temporarily subsidizing a buyer’s rate to make the purchase feasible.

Part 4: Beyond Rates – Other Contributing Factors to the Chill

While mortgage rates are the dominant story, other factors are contributing to the market’s deep freeze.

- Persistent High Home Prices: Despite lower sales volume, national home prices have not collapsed. The Case-Shiller Index has continued to hit new all-time highs into 2024, albeit at a much slower pace of growth. The fundamental lack of supply, exacerbated by the lock-in effect, is preventing a major price correction.

- Economic Uncertainty: Fears of a recession, layoffs in the tech sector, and general economic anxiety have made both buyers and sellers more cautious.

- Inflationary Pressures: While inflation has cooled from its peak, the increased cost of groceries, utilities, and other essentials further strains household budgets, leaving less room for a massive mortgage payment.

- A Structural Shortage: For decades, the U.S. has underbuilt housing relative to population growth. The National Association of Realtors estimated a deficit of 5.5 to 6.8 million housing units between 2018 and 2021. This underlying shortage provides a firm floor under prices, even as demand wanes due to affordability issues.

Read more: Inflation and Interest Rates: How the Fed’s 2025 Policy Is Shaping U.S. Markets

Part 5: Thawing the Freeze – What Could Break the Standoff?

The multi-trillion-dollar question is: how does this end? The market is unlikely to remain in this state of suspended animation forever. Several scenarios could lead to a thaw.

- A Meaningful Decline in Mortgage Rates: This is the most straightforward path to a thaw. If the Federal Reserve begins to cut its benchmark rate, mortgage rates are expected to follow, albeit gradually. Most economists project that rates settling into the 5-6% range could be enough to unlock a significant number of potential sellers and bring buyers back off the sidelines. This would likely increase both sales volume and inventory simultaneously.

- A Shift in Life Circumstances: The lock-in effect is powerful, but life happens. Job relocations, divorces, births, deaths, and other major life events will inevitably force some homeowners to sell, regardless of their mortgage rate. This provides a small, steady trickle of inventory.

- A Sustained Period of Stagnant or Slowly Declining Prices: If home prices were to stagnate or even fall slightly for a prolonged period while incomes continued to grow, it would slowly repair the broken affordability equation. This is a slower, more gradual path to a thaw.

- Innovation in Housing Finance and Policy: There is growing discussion around policy solutions to boost supply, such as zoning reforms to allow for more dense construction, and financial innovations to help with affordability, like shared-equity programs.

Conclusion: Navigating the New Normal

The U.S. housing market is in a period of painful adjustment. The “chill” is a direct consequence of the withdrawal of the unprecedented monetary stimulus that fueled the previous boom. The standoff between buyers and sellers is a rational response to a deeply distorted financial landscape.

For now, the market is characterized by low activity, high costs, and profound frustration. A return to the 3% mortgage rate era is highly unlikely in the foreseeable future. The “new normal” will likely involve higher borrowing costs than what we became accustomed to in the 2010s.

The path forward requires a recalibration of expectations from all parties. Buyers must adjust to higher monthly payments and may need to compromise on location or home features. Sellers must understand that the days of dozens of competing offers may be over, but that well-priced homes in desirable locations can still sell. The thaw will be gradual, not sudden, and its pace will be dictated by the Federal Reserve, the broader economy, and the slow, steady process of rebuilding housing affordability for the next generation.

Read more: GE to Invest $490M to Reshore Washing Machine Production to U.S.

Frequently Asked Questions (FAQ)

Q1: Is the housing market going to crash like in 2008?

A: Most economists believe a 2008-style crash is unlikely. The fundamental dynamics are different. The mid-2000s bubble was fueled by subprime lending, rampant speculation, and a massive oversupply of homes. Today, lending standards are much stricter, household balance sheets are generally stronger, and the primary issue is a critical undersupply of housing, not an oversupply. While prices could decline in some overheated markets, a nationwide collapse is not the consensus view.

Q2: I have a 3% mortgage rate. Should I ever sell?

A: There is no one-size-fits-all answer. The financial cost of giving up that rate is significant. You should only seriously consider selling if a major life event (e.g., a necessary job relocation, a growing family that requires more space, or a divorce) makes a move unavoidable. Before deciding, run the numbers meticulously: calculate your new estimated monthly payment on a potential new home and assess whether it fits comfortably within your budget.

Q3: As a buyer, should I wait for rates or prices to fall?

A: This is the classic “timing the market” dilemma, which is notoriously difficult. If you wait for rates to fall, you may face more competition from other buyers, which could push prices higher. If you wait for prices to fall, there’s no guarantee they will, especially with such low inventory. The best approach is to make a decision based on your personal financial readiness and housing needs. If you find a home you love, can afford the monthly payment, and plan to live there for at least 5-7 years, it can still be a good time to buy, as you can always refinance your mortgage if rates drop in the future.

Q4: Why are home prices still so high if nobody can afford to buy?

A: This speaks to the core paradox of the current market. While “nobody” is an overstatement, demand has certainly shrunk. However, the supply has shrunk even more dramatically due to the lock-in effect. The few buyers who are active are competing for a very small number of available homes, which keeps upward pressure on prices. Furthermore, all-cash buyers and investors, who are immune to mortgage rates, make up a larger portion of the remaining demand.

Q5: What is a mortgage rate buydown and how does it work?

A: A mortgage rate buydown is a financial incentive, often offered by homebuilders or sellers, where they pay an upfront fee to the lender to temporarily or permanently reduce the buyer’s mortgage rate. A common example is a “2-1 buydown,” where the borrower’s interest rate is reduced by 2% in the first year and 1% in the second year, before settling at the permanent note rate for the remainder of the loan. This helps ease the initial payment burden for buyers.

Q6: How does the Federal Reserve influence mortgage rates?

A: The Fed sets the federal funds rate, which is the rate banks charge each other for overnight loans. This influences the yield on the 10-year U.S. Treasury bond. Since mortgages are long-term loans, lenders use the 10-year yield as a benchmark to price them. When the Fed raises its rate to fight inflation, it generally pushes Treasury yields and, consequently, mortgage rates higher. When it cuts rates, the opposite tends to occur.

Q7: Are there any silver linings for buyers in this market?

A: Yes, there are a few. The intense, multiple-offer bidding wars have largely subsided in many areas, giving buyers more time to consider a home and negotiate terms (like inspections and repairs). There is also less pressure to waive all contingencies, which was a common and risky practice during the peak frenzy. Additionally, the rise of builder incentives like rate buydowns can make new construction a more viable and affordable option.