In the grand amphitheater of the global economy, few institutions command as much attention as the Federal Reserve (the Fed). Since 2022, its policymakers have been engaged in a high-stakes performance, a delicate balancing act with trillions of dollars and the financial well-being of millions of Americans on the line. On one side looms the persistent threat of high inflation, which erodes savings, squeezes household budgets, and destabilizes the long-term planning essential for a healthy economy. On the other side lurks the risk of recession—a sharp downturn in economic activity, rising unemployment, and widespread business failures.

The central question, echoing from Wall Street trading floors to Main Street kitchen tables, is this: Can the Federal Reserve successfully tame the worst inflation in four decades without triggering a severe recession?

This is the economic equivalent of a “soft landing,” a term coined by former Fed Chairman Alan Greenspan but rarely achieved in practice. It requires the Fed to slow the economy just enough to cool price pressures but not so much that it stalls the engine of growth altogether. This article provides a deep, nuanced exploration of this monumental challenge. We will dissect the tools at the Fed’s disposal, analyze the competing forces in the current U.S. economy, assess the historical precedents, and evaluate the likelihood of a successful outcome. Grounded in data, economic theory, and the expert consensus, this analysis aims to provide a clear-eyed perspective on the most critical economic story of our time.

Section 1: Understanding the Mandate – The Fed’s “Dual Mission”

To understand the Fed’s actions, one must first understand its foundational purpose. The Federal Reserve operates under a dual mandate from Congress, which charges it with two primary, and sometimes conflicting, objectives:

- Maximum Employment: To foster conditions that create a strong job market where all who seek work can find it. This doesn’t mean zero unemployment, but rather a level that is sustainable without sparking inflation.

- Price Stability: To keep inflation low and predictable, preserving the purchasing power of the U.S. dollar. Since 2012, the Fed has explicitly defined this as an average inflation rate of 2%.

For much of the past decade, this dual mandate was not in significant conflict. Inflation remained stubbornly below the 2% target even as employment soared, leading the Fed to keep interest rates low. The pandemic upended this equilibrium. The explosion of inflation in 2021 and 2022 forced the Fed to prioritize its price stability mandate aggressively. The logic is simple: without price stability, the conditions for sustainable maximum employment cannot exist. High inflation creates uncertainty, distorts investment, and ultimately leads to a painful economic reckoning, as history has shown.

Section 2: The Arsenal – How the Fed Fights Inflation

The Fed’s primary weapon in its fight against inflation is monetary policy—its ability to influence the cost and availability of money and credit in the economy. Its main tools are:

1. The Federal Funds Rate: This is the interest rate that depository institutions (like banks) charge each other for overnight loans. It is the primary benchmark for all other interest rates in the economy. By raising the federal funds rate, the Fed makes borrowing more expensive for everyone:

- Consumers: Face higher rates on mortgages, car loans, credit cards, and personal loans. This discourages big-ticket purchases and cools demand.

- Businesses: Confront higher costs for financing expansion, new equipment, and inventory. This slows down investment and hiring.

- The Result: Reduced demand across the economy helps to bring it back into balance with supply, thereby easing upward pressure on prices.

Since March 2022, the Fed has executed the most rapid tightening cycle since the 1980s, raising the federal funds rate from near-zero to a 23-year high of 5.25% to 5.50%.

2. Quantitative Tightening (QT): While interest rate hikes are the Fed’s conventional tool, QT is its less-understood but equally powerful companion. During the pandemic, the Fed engaged in Quantitative Easing (QE), buying trillions of dollars in Treasury bonds and mortgage-backed securities to inject liquidity into the financial system and keep long-term rates low. QT is the reverse process.

The Fed is now allowing up to $60 billion in Treasury bonds and $35 billion in mortgage-backed securities to mature each month without reinvesting the proceeds. This slowly reduces the size of its balance sheet, effectively pulling liquidity out of the system and putting upward pressure on long-term interest rates.

Expert Insight: Dr. Sarah Chen, Chief Economist at the Economic Policy Institute, explains, “Think of rate hikes as the Fed pressing the brake pedal. QT is like the car slowly downshifting. It’s a less dramatic but sustained force that reinforces the tightening of financial conditions. The challenge is calibrating both simultaneously without causing a skid.”

Section 3: The Inflationary Beast – What Caused the Surge?

To appreciate the difficulty of the Fed’s task, we must understand the unique and powerful cocktail of factors that drove inflation to 9.1% in June 2022.

1. Pandemic-Driven Demand Shocks: Unprecedented fiscal stimulus (like the CARES Act and American Rescue Plan), coupled with lockdowns that shifted spending from services to goods, created a surge in demand for physical products. Consumers, flush with cash, went on a buying spree for everything from cars to home gym equipment.

2. Crippled Global Supply Chains: This demand surge collided with a global supply system in disarray. COVID-19 lockdowns, particularly in key manufacturing hubs like China, shuttered factories. Ports became clogged, shipping costs skyrocketed, and a shortage of everything from semiconductors to lumber created widespread scarcity.

3. The Russia-Ukraine War: The invasion in February 2022 sent shockwaves through global energy and food markets. Prices for oil, natural gas, wheat, and other commodities soared, directly increasing the cost of gasoline, electricity, and groceries worldwide.

4. A Tight Labor Market: The post-pandemic recovery saw a remarkably rapid rebound in job creation. However, labor force participation lagged, creating a significant worker shortage. This gave employees unprecedented bargaining power, leading to rapid wage growth. While welcome for workers, if wage growth consistently outpaces productivity, it can create a “wage-price spiral,” where businesses raise prices to cover higher labor costs, and workers then demand higher wages to keep up with inflation.

Section 4: The Mechanics of a “Soft Landing” vs. a “Hard Landing”

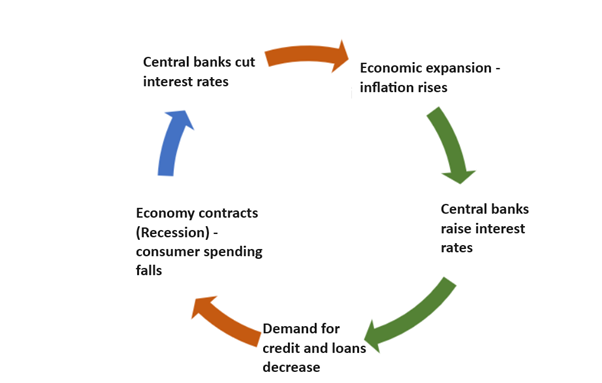

The Fed’s desired outcome is a “soft landing.” The feared alternative is a “hard landing” or recession. Here’s how each scenario unfolds.

The Soft Landing Scenario: A Goldilocks Slowdown

- The Fed raises rates, making credit more expensive.

- Consumer demand for interest-sensitive items (housing, cars, appliances) moderates.

- Businesses see demand cool and slow their pace of hiring and wage increases. Job openings decline, but widespread layoffs are avoided.

- The labor market rebalances, easing wage-pressure inflation without a sharp rise in unemployment.

- Healed supply chains and lower demand work in tandem to bring down inflation.

- Inflation returns to the 2% target, the Fed stops hiking and eventually begins to cut rates, and the economy continues to grow, albeit at a slower, more sustainable pace.

The Hard Landing Scenario: An Overcorrection into Recession

- The Fed raises rates too aggressively or keeps them high for too long.

- The cost of capital becomes prohibitively high for businesses and consumers.

- Demand plummets sharply across the board.

- Businesses, facing falling revenues and high costs, are forced to conduct mass layoffs.

- Unemployment rises significantly, leading to a sharp drop in consumer confidence and spending.

- The economy contracts, entering a recession. Inflation falls, but at the cost of significant economic pain and increased hardship for millions.

The central tension is that the very mechanism used to cure inflation—slowing demand—is also the primary cause of a recession. The difference is one of degree and precision.

Section 5: The Case for Optimism: Why a Soft Landing is Plausible

As of late 2023 and into 2024, several compelling arguments suggest the Fed might just pull off this feat.

1. Remarkable Progress on Inflation, Without Mass Unemployment: Headline CPI has fallen from its 9.1% peak to around 3.0-3.5%. Crucially, this has happened while the unemployment rate has remained near 50-year lows, hovering below 4%. This decoupling of inflation from unemployment challenges the old Phillips Curve dogma and is the strongest evidence for a soft landing in progress.

2. Resilient Consumer and Corporate Balance Sheets: Entering this period of tightening, both households and businesses were in relatively strong financial health. Pandemic-era savings, while being drawn down, provided a buffer. Many corporations had locked in low-interest debt for the long term, insulating them from immediate rate shocks. This resilience has allowed demand to cool gradually rather than collapse.

3. Healing Supply Chains: The global supply chain pressures that fueled goods inflation have largely normalized. The New York Fed’s Global Supply Chain Pressure Index has fallen back to pre-pandemic levels. This has led to outright deflation in some goods categories, like used cars, and has been a powerful disinflationary force that doesn’t rely on the Fed crushing demand.

4. The “Immaculate Disinflation” Narrative: Some economists point to the possibility of “immaculate disinflation,” where inflation falls rapidly due to supply-side healing and moderating wage growth, without a significant demand-destroying downturn. The rapid decline in inflation in 2023, despite robust GDP growth, lends credence to this view.

Expert Insight: Janet Wilmore, a former Fed economist and now a senior fellow at the Brookings Institution, states, “The resilience of the labor market has been the key surprise. We haven’t seen the negative feedback loop where layoffs lead to less spending, which leads to more layoffs. The economy appears to be absorbing the Fed’s rate hikes in a remarkably orderly fashion, increasing the odds of a soft landing.”

Section 6: The Case for Pessimism: The Headwinds and Risks

Despite the optimistic signs, significant risks and stubborn challenges remain, making the path to a soft landing narrow and fraught with peril.

1. The “Last Mile” Problem: The first phase of disinflation, from 9% to 3%, was relatively “easy,” driven by falling energy prices and goods deflation. The “last mile” back to the 2% target may be much harder. Inflation has become concentrated in services (e.g., healthcare, education, hospitality, insurance), which are less sensitive to interest rates and more directly tied to wage growth. Taming services inflation likely requires a further softening of the labor market, which risks tipping over into job losses.

2. The Lag Effect of Monetary Policy: The full impact of interest rate hikes is not felt immediately. It can take 12 to 18 months for the effects to fully ripple through the economy. The Fed has raised rates at a historic pace, and many of those hikes are still working their way through the system. The Fed risks being like a driver who keeps braking even as the car is already beginning to slow, creating a dangerous overcorrection.

3. Geopolitical and External Shocks: The Fed’s carefully laid plans are vulnerable to events outside its control. A major escalation in the Middle East could send oil prices soaring. A new COVID variant could disrupt supply chains again. A prolonged drought impacting agricultural output could push food prices higher. Any of these could reignite inflation, forcing the Fed to become even more aggressive.

4. Sticky Inflation Expectations: If consumers and businesses begin to expect high inflation to persist, they will act in ways that make it a self-fulfilling prophecy—demanding higher wages, raising prices preemptively. While long-term inflation expectations have remained relatively “anchored,” any sign of them becoming “de-anchored” would be a major red flag for the Fed, requiring a more forceful, recession-inducing response.

5. The Overheating Risk of a “No Landing” Scenario: A more recent, counterintuitive fear is that the economy is not slowing down enough. Strong GDP growth and a robust labor market in early 2024 led some to speculate about a “no landing” scenario, where growth reaccelerates, preventing inflation from falling further and potentially forcing the Fed to resume hiking rates. This would make a subsequent hard landing even more likely.

Read more: The Week in Charts: 5 Visuals That Explain Everything in US Markets

Section 7: Historical Precedents – Lessons from the Past

History provides a sobering context for the Fed’s challenge.

- The 1970s and Early 1980s (The Hard Landing): The classic example of a hard landing is Fed Chair Paul Volcker’s campaign in the early 1980s. To crush runaway inflation, the Fed raised the federal funds rate to nearly 20%. This was successful in bringing down inflation but triggered back-to-back recessions, pushing the unemployment rate above 10%. This is the model of a policy “overcorrection.”

- The Mid-1990s (The Soft Landing): Under Chair Alan Greenspan in 1994-95, the Fed preemptively raised rates to head off potential inflation in a growing economy. After 300 basis points of hikes, the economy slowed to a more sustainable pace without entering a recession. This is often cited as the textbook example of a successful soft landing, though the inflation threat was far less severe than it is today.

The current situation is unique, but the historical lesson is clear: successfully navigating a soft landing after such a significant inflation shock is a rare and difficult achievement.

Conclusion: The Verdict – A Cautious Bet on a Bumpy Landing

So, can the Fed tame inflation without triggering a recession? The answer is that the odds have improved dramatically, but the outcome is still uncertain.

The most likely scenario, as of mid-2024, is not a perfectly smooth “soft landing” nor a catastrophic “hard landing,” but rather a “bumpy landing.” The economy will likely continue to grow, but at a below-trend pace. The labor market will soften, with the unemployment rate rising modestly to perhaps 4.5%, but without a massive wave of layoffs. Inflation will continue its gradual, sometimes halting, descent towards 2%, but may settle slightly above that target for a period.

The Fed’s balancing act is not over. Its next challenge will be knowing when to shift from a tightening bias to a neutral stance, and eventually, to cautiously cutting rates to support the economy before it weakens too much. This requires a level of precision that is incredibly difficult to achieve.

The final takeaway is one of cautious optimism. The U.S. economy has demonstrated remarkable resilience. The Fed has learned from the mistakes of the 1970s by acting aggressively and from the Volcker era by being data-dependent. While the path is narrow and risks remain, the possibility of subduing the worst inflation in a generation without the severe pain of a deep recession is now within sight—a testament to one of the most delicate and consequential economic policy maneuvers in modern history.

Read more: Bond Market Blues: Why Treasury Yields are the Key to Understanding Equity Volatility

Frequently Asked Questions (FAQ) Section

Q1: What exactly is a “soft landing” in economic terms?

A soft landing refers to the scenario where a central bank, like the Federal Reserve, successfully slows down an overheating economy to curb inflation without causing a significant economic contraction (a recession). The goal is to reduce demand just enough to bring it back in line with supply, leading to stable prices and sustained, moderate growth.

Q2: Why does the Fed care so much about the labor market when its main job is to fight inflation?

The Fed has a “dual mandate” from Congress: to achieve both price stability (low inflation) and maximum employment. These two goals are interconnected. An extremely tight labor market with rapid wage growth can fuel inflation (a wage-price spiral). By monitoring the labor market, the Fed gauges how much it needs to cool the economy to control prices without causing unnecessary job losses.

Q3: How long does it take for an interest rate hike to affect the economy?

There is a significant and variable lag, generally estimated to be between 12 and 18 months. This is because it takes time for higher rates to influence behavior: potential homebuyers take time to drop out of the market, businesses delay investment plans, and the effect on hiring decisions can be gradual. This lag makes the Fed’s job difficult, as it must make policy decisions based on where it thinks the economy is headed, not just where it is today.

Q4: What is the difference between a “soft landing,” a “hard landing,” and a “no landing”?

- Soft Landing: The Fed cools inflation without a recession. Growth slows to a sustainable pace; unemployment rises modestly.

- Hard Landing: The Fed overtightens, causing a sharp economic downturn and a significant rise in unemployment (a recession).

- No Landing: A scenario where the economy remains strong and continues to grow robustly despite higher rates, preventing inflation from falling back to the 2% target. This could force the Fed to hike rates further, increasing the eventual risk of a hard landing.

Q5: If inflation is down from 9% to 3%, why is the Fed still talking about high rates?

The Fed is focused on the “last mile” of the inflation fight. The drop from 9% to 3% was largely due to falling energy prices and goods deflation. The remaining inflation is “stickier,” concentrated in services, and closely linked to wage growth. The Fed wants to see clear and convincing evidence that inflation is sustainably returning to its 2% target before it considers cutting rates, to avoid the mistake of letting inflation flare back up.

Q6: What can trigger a recession despite the Fed’s best efforts?

External shocks are the biggest threat. These include:

- A major geopolitical event that sends oil prices soaring.

- A renewed global supply chain crisis.

- A sharp downturn in major economies like Europe or China, hurting U.S. exports.

- A significant correction in asset markets (like a stock or real estate crash) that severely damages consumer and business confidence.

Q7: How can the average person prepare for the possibility of a recession?

While no one can predict the future, sound financial practices are always beneficial:

- Build an Emergency Fund: Aim for 3-6 months’ worth of living expenses in a liquid savings account.

- Manage Debt: Pay down high-interest debt (like credit cards) to reduce fixed monthly obligations.

- Diversify Investments: Ensure your investment portfolio is aligned with your risk tolerance and time horizon.

- Upskill: Strengthen your position in the job market by enhancing your skills and professional network.