A specter is haunting the American economy—the specter of stagflation. This ominous term, a portmanteau of “stagnation” and “inflation,” conjures images of the tumultuous 1970s: long gas lines, soaring unemployment, and a pervasive sense of economic malaise that confounded policymakers and crippled household budgets. For decades, the phenomenon was considered a relic of a bygone era, a perfect storm of bad luck and poor policy that modern central banking had consigned to the history books.

Yet, in the wake of the COVID-19 pandemic, massive fiscal stimulus, persistent supply chain disruptions, and the energy market shocks following Russia’s invasion of Ukraine, the word has staged a dramatic comeback. Headlines warn of its return, investors fret over its implications, and consumers feel its pinch at the grocery store and the gas pump. The critical question we face today is whether these fears are a legitimate warning of a repeat of one of America’s most challenging economic periods or a modern-day myth, a simplistic narrative applied to a far more complex and structurally different economic landscape.

This article will delve deep into the anatomy of stagflation, drawing on economic history, data analysis, and expert insight to separate alarmism from credible risk. We will dissect the parallels and divergences between the 1970s and the 2020s, evaluate the current policy responses, and ultimately assess the probability that the U.S. is truly heading for a re-run of that dismal decade.

Part 1: The Ghost of Stagflation Past – Understanding the 1970s

To understand present-day fears, one must first comprehend the original stagflationary episode. The 1970s presented an economic puzzle that defied the prevailing Keynesian orthodoxy, which held that inflation and unemployment were inversely related (a concept known as the Phillips Curve). High inflation was supposed to correlate with low unemployment, and vice versa. Stagflation shattered this belief by delivering the worst of both worlds simultaneously.

The Perfect Storm of the 1970s

The stagflation of the 1970s was not a single event but a series of cascading shocks and deep-seated policy errors.

- The Great Inflation Begins: Loose Monetary and Fiscal Policy

The seeds were sown in the late 1960s. President Lyndon B. Johnson’s “Great Society” programs and the escalating cost of the Vietnam War created massive fiscal deficits, funded not by taxes but by an accommodative Federal Reserve. This “guns and butter” policy flooded the economy with money, stoking demand-pull inflation well before the oil crises. - The Nixon Shock and the End of Bretton Woods (1971)

President Richard Nixon unilaterally suspended the convertibility of the U.S. dollar into gold, effectively ending the Bretton Woods system of fixed exchange rates. This move, intended to address a growing trade deficit, led to a sharp devaluation of the dollar. A weaker dollar made imports—including the crude oil that was priced in dollars—more expensive, importing inflation into the American economy. - The Oil Shocks: OPEC Embargo (1973) and the Iranian Revolution (1979)

The Arab members of OPEC (Organization of the Petroleum Exporting Countries) proclaimed an oil embargo in response to U.S. support for Israel during the Yom Kippur War. The price of oil quadrupled almost overnight. This was a classic cost-push inflation shock. Energy is a fundamental input for virtually every industry; soaring costs rippled through the entire economy, raising the price of production, transportation, and heating. A second, similar shock followed the Iranian Revolution in 1979, doubling oil prices again. - The Productivity Slowdown

U.S. productivity growth, which had been robust in the post-war period, began a pronounced and puzzling decline in the early 1970s. The reasons are still debated but likely include the maturation of the post-WWII technological boom, rising regulatory burdens, and the shift from a manufacturing to a service-based economy. Slower productivity growth meant the economy’s potential output was lower, making it harder to grow without generating inflation. - Wage-Price Spirals and Inflationary Psychology

This was perhaps the most pernicious element. As prices rose, workers demanded higher wages to keep up with the cost of living. Businesses, facing higher wage costs and strong demand, raised their prices further. This created a self-reinforcing wage-price spiral. Crucially, the public began to expect high inflation to continue, embedding it into their financial decisions (e.g., demanding larger annual raises), which made the inflation structurally persistent. - Policy Missteps: The Fed’s “Stop-Go” Approach

Initially, the Federal Reserve, under Chairmen Arthur Burns and later G. William Miller, was reluctant to aggressively fight inflation for fear of triggering a severe recession. They pursued a “stop-go” policy: tightening monetary policy until unemployment began to rise, then quickly loosening again before inflation was fully tamed. This approach only served to entrench inflationary expectations, signaling that the Fed was not truly committed to price stability.

The culmination of this era was the “Volcker Shock.” Appointed Fed Chairman in 1979, Paul Volcker dramatically raised the federal funds rate to unprecedented levels (peaking at nearly 20%), knowingly inducing two deep recessions in the early 1980s. His brutal medicine worked, breaking the back of inflation and, just as importantly, resetting inflation expectations. The cost, however, was severe economic pain and unemployment soaring above 10%.

Part 2: The Modern Economic Landscape – Echoes and Divergences

Fast forward to the post-2020 economy. The parallels are striking enough to cause legitimate concern, but a closer examination reveals profound differences in structure, policy, and context.

The Alarming Parallels

- Supply Shocks: The COVID-19 pandemic and the war in Ukraine served as the modern equivalents of the OPEC embargo. Lockdowns, factory closures, and a shift in demand from services to goods created historic bottlenecks in global supply chains. The Russian invasion of Ukraine then triggered a global energy and food crisis, sending the prices of oil, natural gas, wheat, and other commodities soaring. This was a clear, global cost-push inflation shock.

- Expansionary Macroeconomic Policy: In response to the pandemic, the U.S. government enacted unprecedented fiscal stimulus, including direct checks to households, enhanced unemployment benefits, and business support programs (the CARES Act, American Rescue Plan). Concurrently, the Federal Reserve slashed interest rates to zero and embarked on massive quantitative easing (QE), purchasing trillions of dollars in bonds. The combined effect was a tidal wave of liquidity that supercharged consumer demand just as supply capacity was constrained—a classic recipe for inflation.

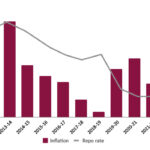

- Rising Inflation: The result was the highest inflation rate in 40 years, with the Consumer Price Index (CPI) peaking at 9.1% year-over-year in June 2022. The public, having not experienced such price surges in decades, began to worry that a new era of high inflation had arrived.

The Critical Divergences

Despite these parallels, the current economic environment is fundamentally different in several key aspects.

- The Central Bank Mandate and Credibility:

- Then: The Fed of the 1970s lacked a clear, unwavering commitment to price stability. Its “stop-go” approach destroyed its credibility.

- Now: Since the Volcker era, the Fed’s primary mandate has been explicitly understood as controlling inflation. Its hard-won credibility is its most powerful tool. Under Chair Jerome Powell, the Fed has embarked on the most aggressive tightening cycle since Volcker, raising rates from zero to over 5% in roughly a year and signaling a commitment to “higher for longer” if necessary. This demonstrates a clear will to crush inflation, even at the risk of a downturn, which helps to anchor long-term inflation expectations.

- Inflation Expectations:

- Then: Expectations became “unanchored,” rising persistently and becoming a self-fulfilling prophecy.

- Now: So far, long-term inflation expectations, as measured by surveys and market-based indicators like the 5-year, 5-year forward breakeven rate, have remained remarkably well-anchored around the Fed’s 2% target. This is a testament to the Fed’s credibility. While short-term expectations spiked, the belief that the Fed will ultimately succeed in bringing inflation down has prevented a 1970s-style wage-price spiral from taking hold.

- Labor Markets and Wage Growth:

- Then: Powerful labor unions, representing a much larger share of the private workforce, had the bargaining power to automatically index wages to inflation via Cost-of-Living Adjustments (COLAs), fueling the spiral.

- Now: Unionization rates are far lower, and the link between inflation and wages is much weaker. While nominal wage growth has been strong in recent years, for much of the post-pandemic period, it has lagged behind inflation, meaning real wages have been negative. This is the opposite of a wage-price spiral. Recently, real wage growth has turned positive as inflation has cooled, but there is little evidence of an uncontrolled, inflationary feedback loop between wages and prices.

- Energy Dynamics and the Green Transition:

- Then: The U.S. was heavily dependent on imported oil, making it acutely vulnerable to OPEC’s decisions.

- Now: The shale revolution has transformed the United States into the world’s largest producer of oil and natural gas. While global prices still affect U.S. consumers, the nation is far more energy-independent. A price spike is less a direct drain on the U.S. economy and more a transfer within it (from consumers in states like California to producers in states like Texas). Furthermore, the growth of renewable energy means the economy is less oil-intensive per unit of GDP than it was 50 years ago, somewhat dampening the impact of oil shocks.

- Demographics and Globalization:

- Then: The post-war baby boom was entering the workforce, and globalization was in its infancy.

- Now: The aging population is a persistent, deflationary force, as older individuals typically consume less. While globalization is facing headwinds (de-risking, reshoring), decades of integrated supply chains have created a level of global competition that still exerts a disinflationary pull, unlike the more insulated economies of the 1970s.

Part 3: Diagnosing the Present – Are We in Stagflation Now?

To answer this, we must return to the strict definition of stagflation: a period of high inflation coupled with stagnating economic growth and rising unemployment.

- Inflation: As of early 2024, inflation has decelerated significantly from its 9.1% peak, falling to the 3-4% range. This is still above the Fed’s 2% target but is a far cry from the persistently double-digit inflation of the late 1970s. The trend is decisively downward.

- Economic Growth: The U.S. economy has defied widespread predictions of a recession. Growth, while moderating, has remained positive. Real GDP grew at a robust 2.5% for all of 2023, and 2024 has seen continued, though slower, expansion. This is the antithesis of “stagnation.”

- Unemployment: The unemployment rate has remained at or below 4% for an extended period, a historically low level that indicates an exceptionally strong labor market.

By the textbook definition, the current situation is not stagflation. It is a period of above-target inflation with resilient economic growth and a tight labor market. Some economists have coined the term “vibeflation” to describe the disconnect between solid macroeconomic data and gloomy public sentiment, while others refer to it as a “rolling recession” affecting different sectors at different times.

However, the risk is not zero. The scenario that could lead to true stagflation would be if inflation proves to be far more persistent than expected, “stuck” well above 3%, while the Fed’s aggressive rate hikes finally tip the economy into a recession, causing unemployment to rise. This is the “soft landing” that the Fed is attempting to engineer—the alternative is either failing to control inflation (a 1970s rerun) or over-tightening and causing an unnecessary recession (a Volcker-style hard landing).

Read more: The Dollar’s Dominance: How a Surging USD is Impacting Multinationals

Part 4: The Policy Response – Learning from History?

The policy response to the current inflationary episode has been markedly different from that of the 1970s, drawing directly on the lessons of that difficult period.

The Federal Reserve: Chair Powell and the Fed have been heavily criticized for being “behind the curve” in 2021, initially dismissing inflation as “transitory.” However, once the persistence of inflation became clear, they pivoted decisively. Their approach has been more akin to Volcker’s resolve than Burns’s hesitation. By front-loading rate hikes and communicating a data-dependent but unwavering commitment to their 2% target, they are trying to avoid the “stop-go” trap and, most importantly, keep inflation expectations anchored.

The Federal Government: Fiscal policy has been a mixed bag. The initial stimulus was undoubtedly a contributor to demand-side inflation. However, later legislation, such as the Inflation Reduction Act, is more nuanced. While its name suggests a fight against inflation, its primary effects are long-term—investing in energy security and domestic manufacturing supply chains—which could reduce cost-push inflationary pressures in the future, but with little immediate anti-inflationary impact.

Conclusion: A Modern-Day Myth, But a Useful Warning

So, is the current fear of 1970s-style stagflation a myth? For the most part, yes. The U.S. economy today is structurally different, its central bank is more credible and proactive, and the data simply does not support the diagnosis. We have high inflation (now moderating) alongside strong growth and employment—a difficult and painful combination for households, but not stagflation.

However, branding these fears a “myth” should not be mistaken for complacency. The fear itself has been a useful, even necessary, warning. It forced policymakers, investors, and the public to confront the real and serious threat of entrenched inflation. It spurred the Fed into aggressive action that has likely prevented a worse outcome. The echoes of the 1970s served as a cautionary tale, reminding us of the devastating and long-lasting consequences of letting the inflation genie out of the bottle.

The path ahead remains narrow and fraught with risk. The Fed’s tightening cycle could still trigger a downturn. Geopolitical shocks could send energy prices soaring once more. Underlying inflation in services could prove stubborn. But the most likely scenario is not a repeat of the 1970s. It is a period of slower growth and a patient, grinding battle by the Fed to restore price stability—a battle that, thanks in part to the ghost of stagflation past, they are now far better equipped to fight.

The greatest lesson of the 1970s is that the cost of defeating inflation rises dramatically the longer it is allowed to fester. The current fears, while perhaps overblown in the immediate sense, have ensured that this lesson has not been forgotten.

Read more: The Weekly Pulse: Can the Bull Run Continue as the Fed’s Decision Looms?

Frequently Asked Questions (FAQ) Section

Q1: What exactly is stagflation?

A: Stagflation is an economic condition characterized by three key elements happening simultaneously: 1) High Inflation (a rapid and broad rise in prices), 2) Stagnating Economic Growth (low or negative GDP growth), and 3) High (and Rising) Unemployment. It is considered a “worst-of-both-worlds” scenario because the typical tools to fight inflation (raising interest rates) can worsen unemployment, and the tools to fight unemployment (lowering rates) can worsen inflation.

Q2: What caused the stagflation of the 1970s?

A: It was caused by a perfect storm of factors:

- Loose monetary and fiscal policy in the late 1960s.

- The end of the gold standard (Bretton Woods), devaluing the dollar.

- Major oil price shocks from OPEC in 1973 and 1979.

- A slowdown in productivity growth.

- A self-reinforcing “wage-price spiral” where rising prices led to demands for higher wages, which in turn pushed prices higher.

- Initial hesitation by the Federal Reserve to aggressively tackle inflation.

Q3: How is the current economic situation similar to the 1970s?

A: The similarities that sparked fear include:

- Major Supply Shocks: The COVID-19 pandemic and the Ukraine war disrupted global supply chains and energy markets, similar to the OPEC embargo.

- Expansionary Policy: Massive government stimulus and central bank easing supercharged demand.

- Surge in Inflation: The U.S. saw its highest inflation rate in 40 years, peaking at 9.1% in June 2022.

Q4: How is today’s economy different from the 1970s?

A: The critical differences are:

- A Credible Federal Reserve: The modern Fed has a strong track record and has acted aggressively to fight inflation, unlike the “stop-go” Fed of the 1970s.

- Anchored Inflation Expectations: The public and markets largely believe the Fed will control inflation, preventing a 1970s-style wage-price spiral.

- A Weaker Link Between Wages and Prices: Lower unionization rates mean wages, while growing, have not kept pace with inflation in the same feedback loop.

- U.S. Energy Independence: The U.S. is now a top oil and gas producer, making it less vulnerable to foreign oil shocks.

- Different Demographics/Globalization: An aging population and global competition are generally disinflationary forces.

Q5: Are we currently in a period of stagflation?

A: By the strict definition, no. While inflation has been high, the U.S. economy has experienced strong economic growth and the unemployment rate has remained at historically low levels (near or below 4%). We are in a period of high-but-falling inflation with a resilient economy, which is not stagflation.

Q6: What would it take for full-blown stagflation to occur today?

A: It would require a scenario where inflation becomes persistently stuck well above the Fed’s 2% target (e.g., above 4-5%) at the same time that the economy enters a recession and unemployment begins to rise significantly. This is the “hard landing” or “soft landing fail” scenario that the Fed is trying to avoid.

Q7: What is the Fed doing to prevent stagflation?

A: The Fed is using its primary tool: interest rates. It has raised the federal funds rate at the fastest pace since the 1980s to cool demand and bring inflation down. By doing so decisively, it aims to avoid the mistake of the 1970s, when the Fed was too timid and allowed inflation expectations to become unanchored.

Q8: Should the average person be worried about stagflation?

A: While a full repeat of the 1970s is unlikely, it is rational to be concerned about high inflation, which erodes purchasing power and savings. However, the current focus should be on the Fed’s ability to engineer a “soft landing” (bringing inflation down without causing a major recession) rather than on the specific threat of stagflation. Monitoring inflation data, job market trends, and the Fed’s policy statements provides a more accurate picture of the economic risks.