If you were to look at the headline U.S. economic data from the surface over the past year, you might see a picture of remarkable resilience. The Gross Domestic Product (GDP) has continued to expand, defying widespread predictions of a recession. The job market remains historically tight, with unemployment hovering near multi-decade lows. Consumer spending, the primary engine of the American economy, has chugged along, seemingly undeterred by global headwinds.

Yet, beneath this veneer of robust health lies a persistent and pernicious problem: inflation. While it has retreated from its four-decade peak in mid-2022, the rate of price increases remains stubbornly above the Federal Reserve’s stated 2% target. This creates a complex and high-stakes predicament for the nation’s central bank, the Federal Reserve (the Fed). The Fed is now caught in a profound dilemma, forced to navigate between two conflicting mandates: fostering maximum employment and stabilizing prices.

This article will dissect this “Fed’s Dilemma” by delving into the most recent U.S. economic data. We will explore the surprising strength of GDP growth, the underlying components fueling it, and the persistent pressures keeping inflation elevated. We will then analyze the Fed’s policy toolkit, the historical context of its current challenge, and the potential paths forward for the U.S. economy. The central question we seek to answer is: Can the Fed successfully engineer a “soft landing”—cooling inflation without triggering a significant economic downturn—or is a period of heightened stagflation or a hard landing inevitable?

Part 1: Deconstructing the GDP Growth Engine

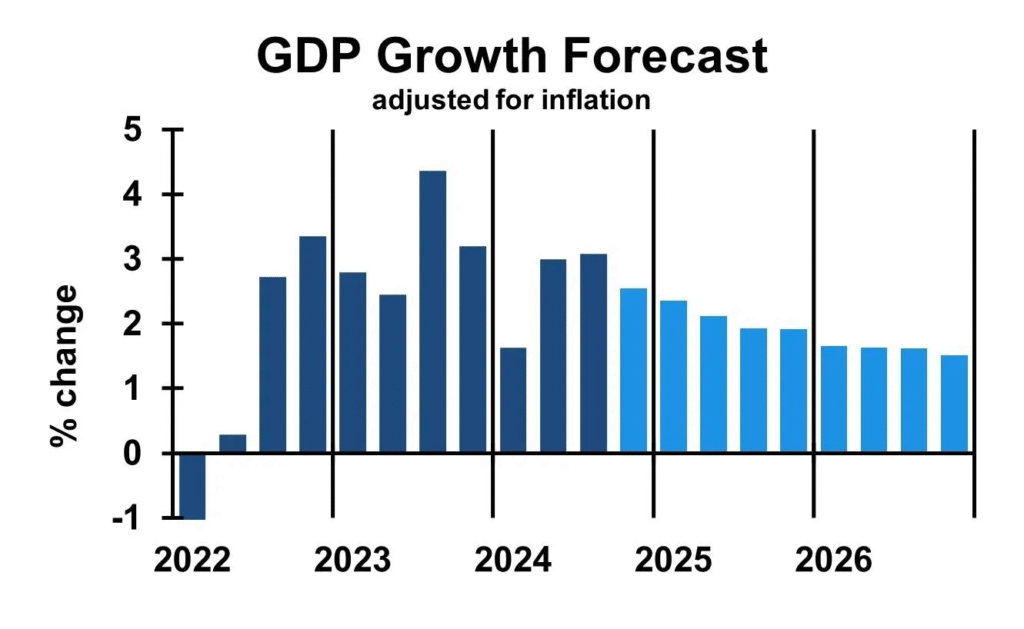

The U.S. economy has demonstrated remarkable fortitude. After a technical recession in the first half of 2022 (two consecutive quarters of negative GDP growth), the economy rebounded strongly. Recent GDP reports have consistently surprised to the upside.

A. The Pillars of Recent GDP Strength:

- Robust Consumer Spending: Accounting for nearly 70% of U.S. economic activity, the American consumer has been the linchpin of growth. This resilience is underpinned by several factors:

- A Strong Labor Market: With unemployment below 4%, wages have been rising, albeit not always at a pace that fully offsets inflation for all demographics. However, the sheer number of people earning paychecks provides a solid foundation for spending.

- Accumulated Savings: During the pandemic, government stimulus and reduced spending opportunities led to a historic buildup of household savings. While this “excess savings” buffer is being depleted, it has provided a cushion against higher prices.

- The “Wealth Effect”: Despite some volatility, asset prices, particularly in housing and the stock market, have remained relatively high, making consumers feel more financially secure and inclined to spend.

- Resilient Business Investment: While softening in some sectors, business investment in equipment and intellectual property products has held up better than expected. Companies, while cautious, continue to spend on technology and automation to boost productivity, especially in a tight labor market.

- Government Expenditure: Fiscal policy has remained expansionary. Legislation such as the Inflation Reduction Act and the CHIPS and Science Act are funneling billions into infrastructure, clean energy, and semiconductor manufacturing, creating jobs and stimulating economic activity.

- A Improving Trade Picture: Net exports have occasionally provided a boost to GDP, as a strong U.S. dollar made imports cheaper and demand for American goods and services abroad remained steady.

B. The Cracks in the Foundation:

However, this growth story is not without its vulnerabilities. The very factors driving GDP are also contributing to the inflationary problem.

- Demand-Pull Inflation: Strong consumer spending directly fuels demand-pull inflation. When demand for goods and services outstrips supply, prices rise.

- Interest-Sensitive Sectors are Slowing: Sectors like housing and durable goods manufacturing have shown significant sensitivity to the Fed’s interest rate hikes. While this is an intended consequence of the Fed’s policy, a deeper slowdown in these areas could eventually spill over into the broader economy.

- The Depletion of Savings: The cushion of pandemic savings is not infinite. As it erodes, consumers may be forced to pull back on spending, potentially creating a drag on growth.

Part 2: The Stubborn Persistence of Inflation

The Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index—the Fed’s preferred gauge—tell a story of inflation that is cooling, but not quickly or uniformly.

A. The Descent from the Peak:

There is no denying the progress made. From a peak of 9.1% year-over-year in June 2022, CPI has fallen significantly. This decline was largely driven by the normalization of goods prices, as supply chains healed and demand shifted back towards services. Prices for used cars, furniture, and other durable goods have stabilized or even fallen.

B. The Sticky Core and Services Inflation:

The real battleground for the Fed now lies in “core” inflation (which excludes volatile food and energy prices) and, more specifically, services inflation.

- Shelter/Housing Costs: This is the single largest component of the CPI. While real-time market data suggests rents for new leases are cooling, there is a significant lag (often 6-12 months) before this shows up in the official inflation data. Shelter costs have been a major, persistent upward force on the inflation indexes.

- Services Inflation Ex-Shelter (Sometimes called “Supercore”): This is where the Fed’s attention is intensely focused. It includes prices for things like healthcare, education, hospitality, and dining out. This category of inflation is particularly worrisome because it is often tightly linked to the labor market.

- The Wage-Price Spiral Concern: In a services-heavy economy, labor is the primary input cost. A tight labor market forces employers to offer higher wages to attract and retain workers. To maintain profit margins, these businesses then raise prices for their services. This can create a self-reinforcing “wage-price spiral,” where rising prices lead to demands for higher wages, which in turn lead to further price increases. While evidence of a full-blown spiral is still debated, the risk is what keeps Fed officials awake at night.

- Sticky Price Components: The Atlanta Fed’s “Sticky Price” CPI, which tracks goods and services that change price relatively infrequently (like medical services and education), has remained elevated, indicating that inflation is becoming more entrenched in the economy’s structure.

Part 3: The Fed’s Toolkit and the Policy Dilemma

The Federal Reserve’s primary tool for managing the economy is the federal funds rate, the interest rate at which banks lend to each other overnight. By raising this rate, the Fed makes borrowing more expensive for everyone—consumers, businesses, and the government. The goal is to cool demand, reduce spending, and thereby bring down inflation.

The Mechanics of the Dilemma:

- The Case for Continued Hawkishness (Fighting Inflation): With core inflation still well above 2%, some economists and Fed officials argue that the job is not done. They fear that pausing or pivoting too soon could allow inflation expectations to become “de-anchored.” If businesses and consumers start to believe that high inflation is permanent, they will act in ways that make it so, creating a much more difficult problem to solve. From this perspective, the Fed must be willing to engineer a period of below-trend growth and higher unemployment to definitively crush inflation, even if it risks a mild recession.

- The Case for a Pivot or Pause (Preserving Growth): On the other side of the argument are those who point to the significant progress already made and the long, variable lags of monetary policy. It can take 12-18 months for the full effect of an interest rate hike to ripple through the economy. The Fed has raised rates at the most aggressive pace since the early 1980s. The argument is that the Fed has already done enough, and continuing to hike risks “over-tightening,” causing an unnecessary and deep recession. They point to the slowing housing market, tightening bank lending standards, and emerging weakness in manufacturing as signs that the medicine is already working.

The “Soft Landing” Aspiration:

The Fed’s stated goal is a “soft landing.” This historical rarity involves tightening monetary policy just enough to slow the economy and cool the labor market, bringing down inflation without causing a sharp rise in unemployment. The most famous example is the mid-1990s under Chairman Alan Greenspan. The current Fed Chair, Jerome Powell, has repeatedly expressed confidence that a soft landing is a plausible outcome, citing the economy’s underlying strength and the fact that labor market rebalancing can occur without a massive spike in joblessness.

Part 4: Analyzing the Data Through the Fed’s Eyes

To understand the Fed’s likely path, we must look at the same data they do, focusing on the interplay between growth and inflation metrics.

- The Jobs Report Jigsaw: The Fed doesn’t just look at the unemployment rate. They scrutinize the Job Openings and Labor Turnover Survey (JOLTS), specifically the ratio of job openings to unemployed persons. A high ratio indicates a tight labor market and upward pressure on wages. A gradual decline in this ratio, without a sharp rise in unemployment, would be a positive sign for a soft landing.

- Productivity Data: If productivity (output per hour worked) is rising, it allows wages to increase without fueling inflation. Strong productivity growth is a key ingredient for a soft landing, as it expands the economy’s potential without stoking price pressures.

- Inflation Expectations: The Fed closely monitors surveys of consumer and business inflation expectations (like the University of Michigan Survey). Well-anchored expectations are a green light for a more patient approach. Rising expectations would be a red flag, likely triggering a more aggressive response.

Part 5: Historical Parallels and the Uniqueness of the Present

History offers some guidance, but no perfect playbook.

- The 1970s Stagflation: The key mistake then was the Fed’s stop-and-go approach—tightening policy to fight inflation, then loosening prematurely when unemployment rose, which allowed inflation to become entrenched. The current Fed is determined to avoid this error, hence its “higher for longer” rhetoric.

- The Volcker Shock of the Early 1980s: To break the back of inflation, then-Chair Paul Volcker raised the federal funds rate to unprecedented levels (peaking near 20%), deliberately inducing a severe recession. The current situation is different, as inflation, while high, started from a much lower base and the Fed has acted more preemptively.

- The Post-2008 Financial Crisis Era: The last decade and a half was characterized by persistently low inflation, which allowed the Fed to keep interest rates near zero. This “low-for-long” period may have created financial imbalances and shaped market psychology in a way that makes the current inflation fight more novel and complex.

The present is unique due to the pandemic’s shock to global supply chains, a massive fiscal response, and a dramatic shift in consumer spending patterns from goods to services. The Fed is navigating uncharted waters.

Read more: Inflation Deep Dive: Analyzing the CPI and PCE Trends in the U.S. Economy

Part 6: Scenarios for the Path Ahead

Based on the current data and the Fed’s stated posture, we can outline several potential scenarios for the U.S. economy:

- The Soft Landing (The Base Case Hope): The Fed executes one or two more modest rate hikes and then holds steady. Growth slows to a below-trend but positive pace, the labor market cools gradually, and core inflation, particularly in services, grinds lower over the next 12-18 months, approaching the 2% target without a recession.

- The Mild Recession (A Plausible Alternative): The cumulative effect of rate hikes finally tips the economy into a short, shallow recession in late 2023 or 2024. Unemployment rises to around 5-6%, which is sufficient to dampen wage growth and break the back of services inflation. The Fed then begins to cut rates to support the recovery.

- Stagflation-Lite (A Significant Risk): Growth stagnates, hovering near zero, but inflation proves far stickier than expected, remaining in the 3-4% range. This would present the Fed with its worst-case scenario: a struggling economy coupled with still-high inflation, leaving it with no good policy options.

- Re-acceleration (The Wild Card): The economy proves even more resilient, and growth re-accelerates, driven by strong consumer balance sheets and fiscal stimulus. This would likely force the Fed to become much more aggressive, raising rates higher than currently anticipated, dramatically increasing the probability of a subsequent hard landing.

Conclusion: Navigating the Narrow Path

The Federal Reserve’s dilemma is a testament to the strange and contradictory nature of the post-pandemic economy. Strong GDP growth and persistent inflation are two sides of the same coin, both born from an economy running too hot, fueled by unprecedented stimulus and a rapid recovery.

The path to a soft landing is exceptionally narrow. The Fed must be both resolute and nimble—resolute in its commitment to restore price stability to prevent a repeat of the 1970s, and nimble enough to recognize when the tightening cycle has done its job to avoid a Volcker-esque downturn. Their success or failure will hinge on the evolution of the labor market and the stubborn components of services inflation.

For businesses, investors, and consumers, the message is one of prepared vigilance. The era of free money is over. Volatility is the new normal. Understanding the delicate balance the Fed is trying to strike—between the undeniable strength of GDP growth and the persistent threat of inflation—is crucial for navigating the uncertain economic landscape ahead. The data in the coming months will reveal whether the Fed’s high-wire act will be remembered as a masterclass in monetary policy or a cautionary tale of the difficulties in taming an overheated economy.

Read more: Decoding the Latest U.S. Jobs Report: Is the Labor Market Cooling or Holding Steady?

Frequently Asked Questions (FAQ)

Q1: Why is the Fed so focused on hitting a 2% inflation target? Why not just accept 3-4%?

The 2% target is not an arbitrary number. It provides a buffer against deflation (a damaging period of falling prices) and creates a stable, predictable environment for long-term planning by businesses and households. Accepting a higher rate risks “de-anchoring” inflation expectations. If people expect 4% inflation, they will demand 5% raises, and businesses will set prices accordingly, creating a self-fulfilling prophecy that can quickly spiral out of control.

Q2: What’s the difference between the CPI and the PCE, and why does the Fed prefer the PCE?

Both measure inflation, but they do so with some key differences. The Consumer Price Index (CPI) is based on a survey of what urban households are buying and is used to adjust Social Security payments. The Personal Consumption Expenditures (PCE) index covers a broader range of spending (including what is paid for by employers or government programs) and its formula is better at capturing how consumers substitute goods when prices change (e.g., buying more chicken if beef gets too expensive). The Fed believes the PCE provides a more accurate and comprehensive picture of inflationary trends across the entire economy.

Q3: What is a “soft landing” and has the Fed ever achieved one before?

A soft landing occurs when the Fed raises interest rates enough to slow the economy and curb inflation without causing a recession. The most celebrated example was in 1994-1995 under Chairman Alan Greenspan. The Fed doubled interest rates from 3% to 6%, successfully cooling inflation and the economy without derailing the long 1990s expansion. It is considered a rare feat of expert macroeconomic management.

Q4: How do higher interest rates actually slow down the economy?

Think of interest rates as the “price of money.” When the Fed raises rates:

- Mortgages and car loans become more expensive, discouraging big-ticket purchases.

- Businesses find it costlier to borrow for expansion, new equipment, or hiring, slowing investment.

- Credit card and variable-rate loan payments increase, reducing consumers’ disposable income.

- The U.S. dollar often strengthens, making American exports more expensive and potentially hurting corporate profits.

This collective cooling of demand eventually reduces the upward pressure on prices.

Q5: If we see a couple of months of negative GDP growth, does that mean we’re in a recession?

Not necessarily. While a common rule of thumb is two consecutive quarters of negative GDP growth, the official declaration of a recession in the United States is made by the National Bureau of Economic Research (NBER). The NBER looks at a broader range of data, including income, employment, industrial production, and retail sales. A recession is defined as a significant decline in economic activity that is spread across the economy and lasts more than a few months. For example, the U.S. had two negative quarters in 2022 but was not declared a recession because the job market remained exceptionally strong.

Q6: What is “core inflation” and why is it so important?

Core inflation strips out the prices of food and energy. These categories are highly volatile—think of oil prices swinging on geopolitical events or food prices shifting due to weather. By focusing on “core” inflation, policymakers try to identify the underlying, sustained trend in inflation. It gives them a better sense of whether inflation is becoming embedded in the economy, which is influenced more by domestic demand and wage growth than by temporary global commodity shocks.

Q7: What can cause a “hard landing” instead of a soft one?

A hard landing, or a significant recession, would likely be caused by the Fed “over-tightening” monetary policy. This could happen if:

- The full, lagged effects of rate hikes hit the economy all at once and with greater force than anticipated.

- A external shock occurs (e.g., a major geopolitical event, a global financial crisis) while the economy is already slowing due to high rates.

- Inflation proves so stubborn that the Fed feels compelled to raise rates to a level that unequivocally breaks the economy’s momentum, leading to a sharp rise in unemployment.