For decades, a core tenet of American economic theory has been that a rising tide lifts all boats. The principle is straightforward: as businesses become more efficient and productive, generating more value per hour of work, the benefits of that increased efficiency would be shared with the workers who made it possible. This symbiotic relationship between productivity and wage growth formed the backbone of the post-World War II American middle class. A worker could reasonably expect that their own economic progress—their ability to afford a home, a car, and a college education for their children—would march in lockstep with the nation’s overall economic advancement.

However, somewhere around the mid-1970s, this fundamental bargain began to fracture. The lines on the graph, which had risen together for generations, started to diverge. Productivity continued its steady climb, fueled by technological innovation, globalization, and new business processes. But wage growth for the typical worker began to stagnate. This “great decoupling” represents one of the most significant and troubling economic trends of the last half-century, contributing profoundly to rising income inequality and widespread economic anxiety.

In this complex landscape, understanding the true state of worker compensation is paramount. Common metrics like average hourly earnings can be misleading, skewed by compositional shifts in the workforce. To cut through the noise, economists and policymakers turn to a more robust and reliable measure: the Employment Cost Index (ECI).

This article provides a comprehensive analysis of the wage-growth versus productivity puzzle, using the ECI as our primary lens. We will explore what the ECI is, why it is the gold standard for tracking labor costs, and what its recent trends reveal about the health of the American worker. We will dissect the historical data, diagnose the causes of the decoupling, and analyze whether recent post-pandemic trends signal a permanent reversal or a temporary anomaly. Our goal is to provide a clear, authoritative, and nuanced understanding of one of the most critical issues facing the U.S. economy today.

Section 1: Understanding the Metrics – ECI, Productivity, and Why They Matter

Before we can analyze the relationship, we must first define our terms with precision. Not all wage data is created equal, and the distinction between productivity and mere output is crucial.

1.1 The Employment Cost Index (ECI): The Gold Standard for Compensation

The ECI is a quarterly economic series published by the U.S. Bureau of Labor Statistics (BLS) that measures the change in the cost of labor, free from the influence of employment shifts among occupations and industries.

Key Features of the ECI:

- It’s an Index, Not a Dollar Amount: The ECI tracks the rate of change in compensation costs, not the absolute level. A value of 120 means costs have risen 20% since the index’s base period (currently December 2005 = 100).

- Comprehensive Compensation: It includes both wages and salaries (straight-time pay, overtime, bonuses, etc.) and benefits (health insurance, retirement plans, paid leave, etc.). This holistic view is critical, as benefits constitute a significant portion of total employee compensation.

- Fixed Weights and Composition Control: This is the ECI’s most important feature. Unlike average hourly earnings, which can be skewed if, for example, a large number of low-wage jobs are lost and then recovered, the ECI holds the occupational and industrial composition of the workforce constant. It asks: “For the same mix of jobs, how much did compensation cost change this quarter?” This makes it the purest measure of wage pressure in the economy.

- Sector Coverage: The ECI data is collected for the private industry and state and local government sectors.

When the Federal Reserve looks for signs of inflationary pressure in the labor market, the ECI is one of the first places it turns. A rapidly rising ECI suggests that employers are being forced to pay more to attract and retain workers, which can feed into broader inflation if businesses pass those costs onto consumers.

1.2 Labor Productivity: Output Per Hour

Labor productivity, also published by the BLS, is a measure of economic performance that compares the amount of goods and services produced (output) with the number of labor hours worked to produce that output.

The Formula:

Productivity = Output / Hours Worked

When productivity increases, it means the economy is generating more value from each hour of labor. This growth is the primary engine for long-term improvements in societal living standards. It can be driven by factors such as:

- Technological innovation (faster computers, automation, new software)

- Increased capital investment (better machinery for workers to use)

- A more skilled and educated workforce

- Efficiencies in scale and production processes

1.3 The Theoretical Link: Why Should Wages Follow Productivity?

In a perfectly competitive market, the theory is clear. The revenue generated by the marginal product of a worker’s labor (the value they add) should determine their wage. If a worker becomes more productive, they generate more value for the firm, and competing employers should be willing to pay a higher wage to secure their services. This competition for labor should, in theory, bid wages up to match the worker’s increased marginal product.

Historically, from the end of World War II until the early 1970s, this is largely what happened. The chart of productivity and compensation (using a measure similar to the ECI) shows two lines moving upward in near-perfect tandem. This period cemented the idea of shared prosperity as a core feature of the American economic model.

Section 2: The Great Decoupling – A Historical Analysis

The period from approximately 1973 to the present day tells a different story—one of divergence and disconnect.

The Data Doesn’t Lie:

According to data from the Economic Policy Institute (EPI), between 1948 and 1979, productivity grew by 108.1%, while compensation for typical workers grew by 93.2%—a relatively close alignment. However, from 1979 to 2022, productivity grew by 64.6%, while compensation for the typical worker grew by just 15.1%. The vast majority of the economic gains generated over the last four decades have accrued to owners of capital and the highest earners, not the median worker.

Visualizing the Gap:

Imagine a graph where both lines start at the same point in 1948. They rise together until the mid-70s. Then, the productivity line continues its ascent, while the compensation line flattens dramatically, creating a widening chasm between them. This chasm represents trillions of dollars in wages that were earned by workers but not paid out to them.

Diagnosing the Divergence: Why Did Wages and Productivity Part Ways?

The decoupling was not caused by a single factor but by a confluence of powerful economic, political, and social forces.

- Globalization and Deindustrialization: The opening of global markets led to the offshoring of millions of manufacturing jobs, particularly those with middling skill requirements and high pay. This placed downward pressure on the wages of similar jobs that remained in the U.S., as workers now competed with a global labor pool willing to work for far less.

- Technological Change and Skill-Biased Technical Change: While technology boosts overall productivity, it hasn’t always benefited all workers equally. Automation and computerization began to replace routine manual and cognitive tasks. This “hollowed out” the job market, increasing demand for high-skill, high-wage analytical jobs and low-skill, low-wage service jobs, while reducing opportunities in the middle. The premium for a college education soared, leaving non-college-educated workers behind.

- The Decline of Labor Unions: Union membership in the private sector has plummeted from over 30% in the 1950s to about 6% today. Unions historically gave workers collective bargaining power to claim a larger share of productivity gains. Their decline has shifted power decisively toward employers, reducing workers’ ability to negotiate for higher wages and better benefits.

- Changes in Corporate Governance and the Rise of Shareholder Primacy: Starting in the 1980s, a new ideology took hold in corporate America: that the primary, and sometimes sole, duty of a corporation is to maximize shareholder value. This led to a focus on short-term stock performance, cost-cutting (often in the form of labor), stock buybacks, and soaring executive compensation—all of which came at the expense of investment in workers and wage growth.

- Erosion of the Minimum Wage and Labor Standards: The federal minimum wage has not kept pace with inflation, let alone productivity growth. Its real value today is significantly lower than it was in 1968. This has pulled down wages at the bottom of the distribution and weakened the bargaining power of low-wage workers more broadly.

Section 3: The ECI in the Post-Pandemic Era – A New Dawn for Workers?

The COVID-19 pandemic triggered an economic earthquake unlike any other, leading to a labor market that has been both extraordinarily tight and a central focus of economic policy. In this unprecedented environment, the ECI has taken on renewed significance.

3.1 The “Great Resignation” and Wage Pressure

Beginning in mid-2021, the U.S. witnessed a historic surge in job quits, as workers, reassessing their lives and careers, left their jobs in record numbers. This massive churn, coupled with a rapid economic rebound and reduced labor force participation, created an extreme imbalance between labor demand and supply. Employers were desperate to hire.

This dynamic was vividly captured by the ECI. After years of relatively modest quarterly increases (often around 0.6-0.8%), the ECI for private industry workers began to spike.

- Q4 2021: +1.3% (Quarterly change)

- Q1 2022: +1.4%

- Q2 2022: +1.4%

These were the largest quarterly increases in the ECI’s history, signaling intense wage pressure across the economy. For the first time in decades, workers had significant leverage, and they used it to command higher pay, particularly in lower-wage sectors like leisure and hospitality, retail, and warehousing.

3.2 Interpreting the Recent Cooldown

Through 2023 and into 2024, as the Federal Reserve aggressively raised interest rates to combat inflation, the labor market has cooled from its white-hot state. The ECI has reflected this moderation.

- Q4 2023: +0.9%

- Q1 2024: +1.2% (A slight re-acceleration that caught economists’ attention)

- Q2 2024: +0.9%

The Critical Question: Is this cooldown a return to the pre-pandemic stagnation, or is it a normalization to a higher plateau of sustainable wage growth?

A Nuanced Interpretation:

- Wage Growth is Still Above Pre-Pandemic Norms: While down from the 2022 peaks, the recent ECI readings of around 0.9% quarterly (which annualizes to roughly 3.6-3.7%) are still meaningfully higher than the ~2.5% annual growth that was common in the 2010s.

- The Composition of Growth is Shifting: The initial surge was led by wages for non-supervisory workers in service industries. More recently, wage growth has become more broad-based, with stronger gains now appearing in professional and business services, as well as in unionized industries where multi-year contracts are catching up to past inflation.

- The Role of Benefits: The ECI’s benefits component has also seen significant increases, driven by rising costs of health insurance and a renewed employer focus on retirement benefits to attract talent. This is a crucial part of the total compensation story that often gets overlooked.

3.3 The Productivity Wildcard

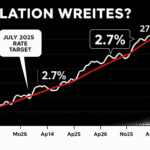

A fascinating development has been the recent surge in productivity data. After a long period of sluggish growth, productivity increased by a remarkable 2.7% in 2023. Early 2024 data also suggests a strong pace.

This raises a tantalizing possibility: What if productivity growth is finally accelerating to meet the new, higher level of wage growth?

There are plausible reasons for this:

- Widespread Adoption of New Technologies: The pandemic forced the rapid adoption of remote work technologies, automation, and AI tools. After an initial adjustment period, businesses are now learning to use these tools more effectively, boosting output per hour.

- Efficient Job Matching and Remote Work: Remote work may allow for more focused, deep work for certain professions, potentially boosting output.

- Capital Investment: Strong business investment in equipment and software in recent years may now be paying dividends in efficiency.

If this productivity surge is sustained, it would validate the recent wage gains. Higher wages would be supported by higher output, rather than simply being an inflationary pressure that forces the Fed to clamp down. This is the optimistic scenario for a return to shared prosperity.

Section 4: The Road Ahead – Implications for Policy, Business, and Workers

The relationship between wage growth and productivity is not a law of nature; it is a function of policy, market structure, and corporate behavior. The recent data provides a potential inflection point, but its sustainability is not guaranteed.

Policy Implications:

- The Federal Reserve’s Dilemma: The Fed’s mandate is price stability and maximum employment. A key question is what level of wage growth is consistent with its 2% inflation target. If productivity is growing at 2-3%, then wage growth of 4-5% can be sustainable without fueling inflation (as unit labor costs would rise only 1-2%). The Fed must therefore carefully monitor both the ECI and productivity data to avoid overtightening and snuffing out a genuine recovery for worker pay.

- Labor Market Policies: Policies aimed at strengthening worker bargaining power—such as supporting unionization, enforcing non-compete and collusion bans, and raising the minimum wage—can directly help to close the productivity-pay gap by ensuring workers have more leverage to claim their share.

- Investment in the Drivers of Productivity: Sustained productivity growth requires public and private investment in R&D, infrastructure, and education. Policies that foster innovation and build a highly skilled workforce are essential for lifting the long-term potential of the economy.

Business Implications:

- The New Talent Equation: The pandemic reset worker expectations. To attract and retain talent in a competitive market, businesses cannot rely on the old playbook. They must offer competitive total compensation (wages and benefits), flexible work arrangements, and a positive culture. Investing in employees is no longer just a cost; it’s a strategic imperative for maintaining a productive workforce.

- Efficiency through Technology: The pressure to pay higher wages will continue to drive investment in automation and AI. The challenge for businesses is to deploy these technologies in a way that augments human labor and creates new, higher-value roles, rather than simply displacing workers.

Read more: Commodities and Currency Movements Affecting Markets

Worker Implications:

- Bargaining Power is Real, But Fragile: The recent period demonstrated that when the labor market is extremely tight, workers can achieve significant gains. However, this power is contingent on the economic cycle. Workers must leverage these periods to secure not just one-time raises but also better benefits, training opportunities, and career paths.

- The Need for Lifelong Learning: As the pace of technological change accelerates, the skills that drive productivity are constantly evolving. Workers must proactively engage in upskilling and reskilling to remain valuable and ensure their own wages can grow alongside productivity.

Conclusion: Reforging the Link?

The decades-long divergence between wage growth and productivity has been a central driver of economic inequality and a source of deep-seated frustration for the American workforce. The Employment Cost Index has been the most reliable tool for documenting the stagnation of compensation for the typical worker.

The post-pandemic period has injected a new dynamic into this long-running story. A powerful, if potentially transient, rebalancing of labor market power led to a historic surge in wage growth, as captured by the ECI. The critical question for the future of the American standard of living is whether this is a temporary blip or the beginning of a new trend.

The answer lies in the interplay of three forces:

- The sustainability of productivity gains from new technologies and work models.

- The enduring strength of worker bargaining power in the face of potential economic slowdowns and automation.

- The policy choices made by governments and corporations.

The great decoupling was not an inevitability; it was the result of a series of choices. Reforging the link between wage growth and productivity will require a conscious and sustained effort across society. It will require policies that foster broad-based growth, business models that view workers as assets to be developed rather than costs to be minimized, and a continued focus on the innovations that drive the economic pie to grow. The latest ECI data offers a glimmer of hope that, after half a century, the fundamental bargain of American capitalism may be open for renewal.

Read more: Volkswagen Courts Trump Administration for Tariff Deal

Frequently Asked Questions (FAQ)

Q1: I keep hearing about “real wages.” What’s the difference between the ECI and real wage growth?

- A: The ECI, as published, is a nominal measure. It tells you how much compensation costs have increased in current dollars. Real wage growth adjusts nominal wage growth for inflation. To calculate it, you subtract the rate of inflation (typically using the Consumer Price Index) from the rate of nominal wage growth. For example, if the ECI for wages and salaries rises 4.5% over the year, but inflation is 3.0%, then real wage growth is 1.5%. This is what truly matters for purchasing power.

Q2: If the ECI is so good, why do I hear about “average hourly earnings” on the news so much more often?

- A: The Average Hourly Earnings (AHE) data is released monthly as part of the BLS’s Current Employment Statistics (CES) survey, making it more timely than the quarterly ECI. It provides a quick, useful snapshot of the labor market. However, as explained, it can be volatile and distorted by shifts in the composition of the workforce. The ECI is released with a one-month lag after the quarter ends but is considered more accurate for underlying wage trends. Serious economists use both, but they rely on the ECI for a purer read on wage pressure.

Q3: Has the productivity-wage gap affected all workers equally?

- A: Absolutely not. The gap is most pronounced for middle- and low-wage workers and those without a college degree. The divergence is a primary cause of rising income inequality. In contrast, the highest earners—particularly the top 1% and 0.1%, whose income comes largely from capital (investments, stock options) and executive pay—have seen their compensation soar, often even faster than productivity growth. They have captured a disproportionate share of the economic gains.

Q4: How does the rise of benefits like health insurance factor into this discussion?

- A: This is a crucial point. The ECI includes benefits, and their cost has risen significantly over the decades, particularly health insurance. This means that total compensation (wages + benefits) has grown faster than wages alone. However, even total compensation has significantly lagged productivity since the late 1970s. Furthermore, a dollar spent on health insurance premiums does not feel the same to a worker as a dollar in their paycheck; it doesn’t increase their disposable income or their ability to pay for housing, food, or education.

Q5: Can Artificial Intelligence (AI) help close the productivity-wage gap?

- A: AI is a double-edged sword. Its potential to dramatically boost productivity is enormous, which could, in theory, provide the economic surplus needed to fund higher wages across the board. However, the distribution of those gains is uncertain. If AI primarily automates and displaces a wide range of cognitive tasks, it could further suppress wage growth for many and exacerbate inequality. The outcome will depend on how AI is implemented (as a tool for workers or a replacement), how the benefits are shared through policy and corporate practice, and how well the workforce adapts with new skills.

Q6: What can I, as an individual employee, do to ensure my wages keep up with productivity?

- A: On an individual level, your personal productivity is your strongest lever.

- Upskill Continuously: Acquire skills that are in high demand and complement new technologies.

- Understand Your Value: Research salary data for your role, industry, and location to ensure you are being paid market rates.

- Negotiate Effectively: Use your documented skills, performance, and market data as leverage during salary reviews.

- Consider Collective Action: Explore unionization with your colleagues if you are in a suitable industry, as collective bargaining has historically been one of the most effective ways to secure a fair share of productivity gains.

Sources & Further Reading:

- U.S. Bureau of Labor Statistics (BLS) – Employment Cost Index

- U.S. Bureau of Labor Statistics (BLS) – Productivity and Costs

- Economic Policy Institute (EPI) – “The Productivity–Pay Gap”

- Federal Reserve Bank of St. Louis (FRED) – Economic Data

- Congressional Research Service (CRS) Reports