The FTSE 100 (^FTSE) and European stocks gained ground on Monday by the closing bell in London, while US stocks were mixed in what is typically one of the quietest trading weeks of the year.

Wall Street is already looking ahead to key inflation reports later this week: the producer price index (PPI) on Wednesday and the consumer price index (CPI) on Thursday. Together, the data will offer fresh insight into the strength of the economy after last week’s softer-than-expected August jobs print, as questions about recession start to emerge.

The moves higher came following the latest trade balance figures released by China, revealing the impact US tariffs have had on exports.

Chinese exports rose 4.4% compared with the previous year, the figures showed, missing economists’ expectations. This was a dip from July’s better-than-expected 7.2% rise. Imports were 1.3% higher, down from a 4.1% rise in July.

Strikingly, shipments to the US fell by 33% and exports to southeast Asian nations rose by 22.5%.

Read more: Trending tickers: Robinhood, Tesla, Alibaba, BP and Marks & Spencer

- The FTSE 100 (^FTSE) gained 0.2% by the end of the session. Marks & Spencer (MKS.L) and Fresnillo (FRES.L) were among the top gainers in the index.

- The DAX (^GDAXI) in Germany rose 0.9% following data German industrial production had risen by 1.3% in July.

- Over in Paris, the CAC 40 (^FCHI) gained 0.8%.

- The pan-European STOXX 600 (^STOXX) rose 0.5%.

- Sterling rose 0.3% against the dollar (GBPUSD=X) ticking above the $1.35 mark. The US dollar index (DX-Y.NYB) — which tracks the greenback against a basket of six currencies — fell 0.2%.

- By mid-morning, the Dow Jones Industrial Average (^DJI) had risen 0.2%, while the S&P 500 (^GSPC) rose 0.4% and the tech-heavy Nasdaq (^IXIC) jumped 0.7%.

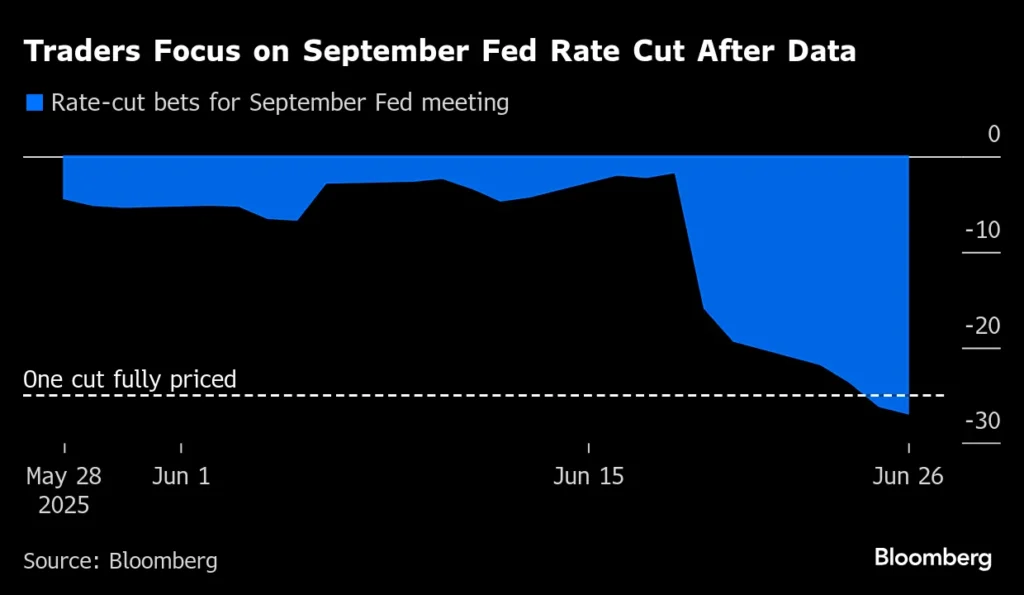

- In terms of the Federal Reserve, the debate now centres on how deep policymakers will cut, amid rising expectations for a bumper “catch-up” move of 50 basis points, rather than 25 basis points.